The commercial real estate crisis looms larger than ever as high office vacancy rates continue to plague major cities across the United States. With businesses adapting to new work models post-pandemic, demand for office space has plummeted, leaving many buildings empty and property values in a freefall. Economists are increasingly concerned about the economic impact of real estate, particularly as large swathes of commercial mortgage debt are set to mature by 2025. This situation raises critical questions about banking system stability as regional banks may struggle under the weight of substantial losses tied to real estate loans. The financial risks in commercial real estate create a turbulent landscape that could have far-reaching repercussions for the broader economy, prompting urgent discussions about potential solutions and interventions.

As we navigate the current turmoil in the property market, the term “commercial real estate downturn” captures the complexities of this evolving financial landscape. The surge in office vacancies, exacerbated by a lasting shift in work culture, denotes a stark transformation in demand for physical workspaces. This upheaval not only threatens the stability of financial institutions but also highlights the broader implications for economic dynamics. Investors and stakeholders are acutely aware that the existing real estate loans may become a ticking time bomb, especially with looming deadlines approaching in 2025. Understanding the multifaceted risks associated with this downturn is crucial for developing strategies that mitigate potential economic fallout and bolster confidence in the banking system.

Understanding the Impact of High Office Vacancy Rates

High office vacancy rates pose a significant risk to economic stability, reflecting a shift in demand for commercial real estate. The ongoing effects of remote work and hybrid employment models have led to a substantial decline in the need for traditional office spaces. In cities like Boston, vacancy rates range from 12 to 23 percent, bringing down property values and straining financial institutions tied to commercial loans. As the demand wanes, the financial repercussions extend beyond the real estate market, triggering concerns about the overall economic landscape.

Moreover, these high vacancy rates can exacerbate the ongoing commercial real estate crisis by leading to increased financial instability. With many businesses downsizing or opting for flexible work arrangements, the future of office buildings remains uncertain. This situation not only affects property owners but also banks and investors that have substantial stakes in commercial real estate, particularly when one considers that 20 percent of the $4.7 trillion in commercial mortgage debt is maturing this year. Should this trend continue, we may see a ripple effect that impacts consumer confidence and spending.

Commercial Real Estate Crisis: Causes and Consequences

The commercial real estate crisis is multifaceted, a concern for financial analysts and policymakers alike. At its core are the high levels of indebtedness among real estate investors, many of whom over-leveraged during a period of low interest rates. As interest rates rise, the financial strain of servicing these debts becomes more pronounced. By 2025, a significant influx of commercial real estate loans will come due, amplifying fears of widespread delinquencies that could destabilize the banking system.

Kenneth Rogoff emphasizes that while some regional banks may face dire consequences, it is unlikely that we will see a full-fledged financial meltdown akin to 2008. Still, the potential for significant losses among pension funds and regional banks raises alarms about the interconnectedness of commercial real estate and the broader economy. This crisis highlights the intricate balance between banking system stability and the economic impact of real estate, as financial risks in commercial real estate could infiltrate other sectors if not managed correctly.

The Relationship Between Interest Rates and Real Estate Loans

Interest rates are a critical factor influencing the stability of the commercial real estate market. The Federal Reserve’s hesitance to lower rates has resulted in a challenging environment for those holding real estate loans, especially as many loans are set to mature by 2025. Investors who previously operated under the assumption that low rates would persist now find themselves in a more precarious position as rates rise, increasing the cost of refinancing.

As Kenneth Rogoff notes, the adjustment process will likely involve a wave of bankruptcies as firms struggle to meet their financial obligations. This realignment, while painful for some investors, is essential for establishing a more sustainable real estate market. The threat of widespread defaults could lead to tighter lending conditions, affecting not only commercial real estate but the broader economy, as banks reassess their risk exposure amid rising financial uncertainties.

Financial Risks in Commercial Real Estate: A Cautionary Outlook

The financial risks accompanying the commercial real estate sector cannot be overstated, especially as high office vacancy rates contribute to declining property values. Many investors are now questioning their commitments, fearing that the market may not recover in time to prevent substantial losses. The structural challenges in converting vacant office spaces into residential units, primarily due to engineering and zoning hurdles, only compound these risks, making the situation more critical.

As we look toward 2025 and beyond, the crucial question for investors and lenders alike is how to navigate this evolving landscape. An increase in delinquent loans could lead to a cascade of issues for regional banks, which are particularly vulnerable compared to their larger counterparts. If left unaddressed, these risks could undermine banking system stability, tightening credit conditions for consumers and businesses across the nation.

How Economy and Real Estate Interact Amidst the Crisis

The intertwining of the economy and the commercial real estate sector is especially evident during periods of crisis. While high vacancy rates and declining property values may suggest an impending economic downturn, it’s vital to recognize that the overall economy remains resilient. This paradox becomes clearer when observing that robust job markets and strong stock performances have yet to translate into widespread economic distress, despite the struggles faced within the real estate market.

Nevertheless, should a major recession hit, consumers may feel the tremors from the commercial real estate crisis in the form of reduced lending and consumption. As regional banks grapple with losses on real estate loans, the ramifications could extend beyond their balance sheets, affecting local economies and overall consumer sentiment. Thus, monitoring the health of the commercial real estate market is critical for understanding potential threats to economic stability.

Potential Solutions to the Commercial Real Estate Crisis

Addressing the commercial real estate crisis requires a multifaceted approach, with emphasis on the necessity for policy interventions that foster refinancing options. While immediate relief such as lowered long-term interest rates could alleviate some of the pressure on borrowers, predicting such an outcome remains challenging in the current economic landscape. Investors must prepare for potential bankruptcies and a restructuring of the industry as it adapts to new market conditions.

Furthermore, enhancing collaboration between banks, borrowers, and regulatory bodies will play a crucial role in navigating the complexities of the commercial real estate market. By implementing more flexible financing options and fostering innovation in property utilization, the sector can begin to recover from the looming crisis. Ultimately, engaging in these discussions will be key to ensuring banking system stability while mitigating economic impacts.

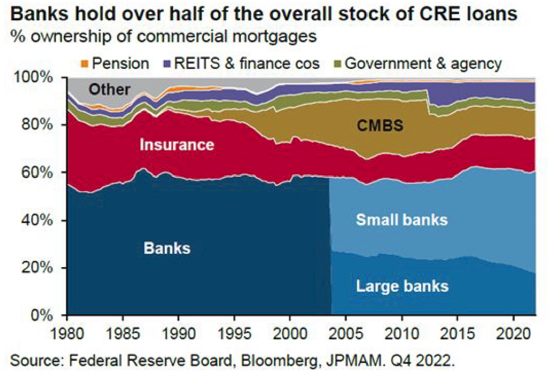

The Role of Regional Banks in the Crisis

Regional banks are at the forefront of the commercial real estate crisis, facing unique challenges due to their concentrated exposure to this market. Unlike larger banks that have diversified their portfolios, smaller institutions may struggle to absorb losses from delinquent loans, especially as high office vacancy rates impede potential recovery. This situation raises concerns about the banking system’s stability amidst a broader economic context.

As some regional banks contend with the fallout from commercial real estate investments, it becomes evident that the risk of failure could have cascading effects throughout local economies. Reduced lending capacity may stymie economic growth, affecting small businesses and consumer spending. It’s imperative to closely monitor the resilience of these banks and develop strategies to safeguard against potential crises, ensuring that they remain viable players in the financial landscape.

The Future of Commercial Real Estate and Recovery Prospects

Looking ahead, the future of commercial real estate remains uncertain, but best practices can be established to support recovery in the sector. Investors must recalibrate their strategies, emphasizing adaptability and innovation in order to remain viable in a changing landscape. This might involve exploring new uses for existing properties or investing in high-demand sectors that continue to show growth, such as logistics and warehousing.

Recovery will also hinge on a favorable economic climate and market conditions. If interest rates eventually decrease, refinancing opportunities may arise, providing some relief to distressed properties. However, stakeholders must remain vigilant in evaluating market dynamics, as the interplay between banking system stability and commercial real estate will continue to shape the economic environment in the years to come.

Navigating the Lending Landscape Amidst Economic Change

In an environment characterized by high office vacancy rates and financial uncertainty, navigating the lending landscape will be vital for both borrowers and banks. Lenders must reassess their risk exposure, particularly in sectors of commercial real estate that are faltering. Adapting lending criteria to align with market realities, while still supporting viable businesses, is crucial to mitigate potential losses.

Additionally, establishing clear communication channels between banks and borrowers will enhance collaboration and foster trust in a turbulent market. Banks should consider developing tailored financing solutions that accommodate the unique needs of each sector within commercial real estate. By doing so, they may not only protect their interests but also contribute to a more resilient economic landscape.

Frequently Asked Questions

How could high office vacancy rates contribute to the commercial real estate crisis in 2024?

The ongoing high office vacancy rates, currently between 12% and 23% in major U.S. cities, are a key factor in the commercial real estate crisis. As businesses adopt remote and hybrid work models, demand for office space has declined significantly. This trend depresses property values, leading to financial instability among property owners and investors, which can exacerbate the existing commercial real estate crisis.

What economic impact could the commercial real estate crisis have in the near future?

The economic impact of the commercial real estate crisis could be significant due to the potential for rising delinquencies on the $4.7 trillion in commercial mortgage debt. If many loans mature without refinancing options, it could lead to widespread bank losses and tighter lending conditions, negatively affecting regional economies and consumer spending.

Will the banking system’s stability be threatened by the commercial real estate crisis?

While concerns exist about banking system stability due to the commercial real estate crisis, major banks are better prepared than they were in previous financial crises. Their diversified portfolios and profitability in other sectors may help mitigate risks. However, smaller regional banks, heavily invested in commercial real estate, may face greater vulnerabilities if significant delinquencies occur.

What are the financial risks in commercial real estate as we approach 2025?

As we approach 2025, the commercial real estate sector faces notable financial risks, primarily due to a surge in loans coming due. With many properties underperforming and values decreasing, investors may struggle to refinance these loans, potentially triggering defaults that could deepen the commercial real estate crisis.

How are real estate loans in 2025 expected to affect the commercial real estate market?

The anticipated wave of real estate loans maturing in 2025 is expected to have a profound impact on the commercial real estate market. With high vacancy rates and reduced property values, borrowers may find it challenging to secure refinancing, which could lead to an increase in foreclosures and an exacerbation of the commercial real estate crisis.

What should investors consider regarding the commercial real estate crisis and their investments?

Investors should closely assess the current trends in commercial vacancy rates and the broader economic environment as they relate to the commercial real estate crisis. The potential for increased delinquencies on loans and the resulting financial instability in the market could impact the value of their investments, making it crucial to consider risk management strategies.

Are there strategies to mitigate the commercial real estate crisis’s effects on the economy?

To mitigate the effects of the commercial real estate crisis on the economy, potential strategies include advocating for lower long-term interest rates to encourage refinancing and supporting policies that facilitate the conversion of vacant office space into residential properties, although the latter presents significant challenges.

What role do regional banks play in the commercial real estate crisis?

Regional banks play a critical role in the commercial real estate crisis as they often hold a substantial amount of debt linked to lower-tier commercial assets. Their potential exposure to losses from these investments could lead to regional economic repercussions, particularly if lending becomes more stringent as banks respond to rising delinquency rates.

How does the commercial real estate crisis impact consumers?

Consumers may experience indirect impacts from the commercial real estate crisis through tighter lending conditions and the potential for reduced employment opportunities in sectors related to real estate. Additionally, losses incurred by pension funds invested in commercial properties may affect individual retirement savings.

What future trends should be closely watched regarding the commercial real estate crisis?

Future trends to monitor include changes in occupancy rates, new policy directives related to interest rates, and the performance of regional banks in response to commercial real estate loan delinquencies. Observing these indicators can provide insights into how the crisis will evolve and its broader economic implications.

| Key Point | Details |

|---|---|

| High Vacancy Rates | Office building vacancy rates remain high, ranging from 12% to 23% in major U.S. cities, impacting property values. |

| Surge of Commercial Real Estate Loans | 20% of $4.7 trillion in commercial mortgage debt is due this year, raising concerns of bank delinquencies and failures. |

| Economic Impact | Possible widespread bank losses could rattle the broader economy, but a full-blown financial crisis is not expected. |

| Diminished Demand | Post-pandemic, demand for office space has declined, with current occupancy rates averaging around 50%. |

| Over-Leveraging | Investors over-leveraged during low-interest rates, making them vulnerable to the current economic climate. |

| Pension Fund Exposure | Pension funds heavily invested in commercial real estate may suffer significant losses. |

| Regional Banks at Risk | Smaller banks are more susceptible to impacts from commercial real estate losses, which could affect regional economies. |

| Comparison to 2008 Crisis | Current market conditions, despite challenges, differ significantly from those leading to the 2008 financial crisis. |

Summary

The commercial real estate crisis is poised to have significant implications for the economy, particularly as high office-vacancy rates may lead to widespread bank losses in the upcoming years. With roughly twenty percent of commercial mortgage debt due this year, the potential for defaults looms large, raising alarms among financial experts. While larger banks are better prepared due to strict regulations post-2008 and continue to perform well overall, regional banks could face severe repercussions, affecting local economies. The slow recovery in demand for office space, combined with high-interest rates and past over-leveraging, contributes to a precarious situation. However, a catastrophic financial meltdown similar to 2008 is not anticipated unless additional economic shocks occur.