Corporate tax rates have become a focal point in the ongoing debate over fiscal policy and economic growth. With the expiration of key provisions from the 2017 Tax Cuts and Jobs Act (TCJA) looming, legislators are gearing up for a contentious battle over whether to raise or cut taxes. Proponents of tax cuts argue that lowering the corporate tax rate stimulates business investments, creating jobs and, ultimately, boosting corporate tax revenue. In contrast, advocates for higher corporate tax rates suggest that such measures could enable governments to fund essential services and reforms, including the expanded Child Tax Credit. As this delicate balancing act unfolds, understanding the implications of corporate tax rates on the economy will be crucial for voters and policymakers alike.

The discussion surrounding business taxation, particularly corporate tax obligations, is heating up as the policy landscape shifts. As the expiration of multiple provisions from the TCJA draws near, lawmakers are assessing whether to implement tax increases or maintain existing cuts. Supporters of lower corporate tax obligations maintain that reducing these rates is vital for stimulating capital expenditures and spurring overall economic growth, while detractors emphasize the need for a stable revenue framework. Additionally, the renewed conversation about the Child Tax Credit and its effects on families highlights the broader ramifications of corporate taxation on social programs. This complex interplay between taxation, investment, and economic vitality is sure to shape the future landscape of fiscal policy in the years to come.

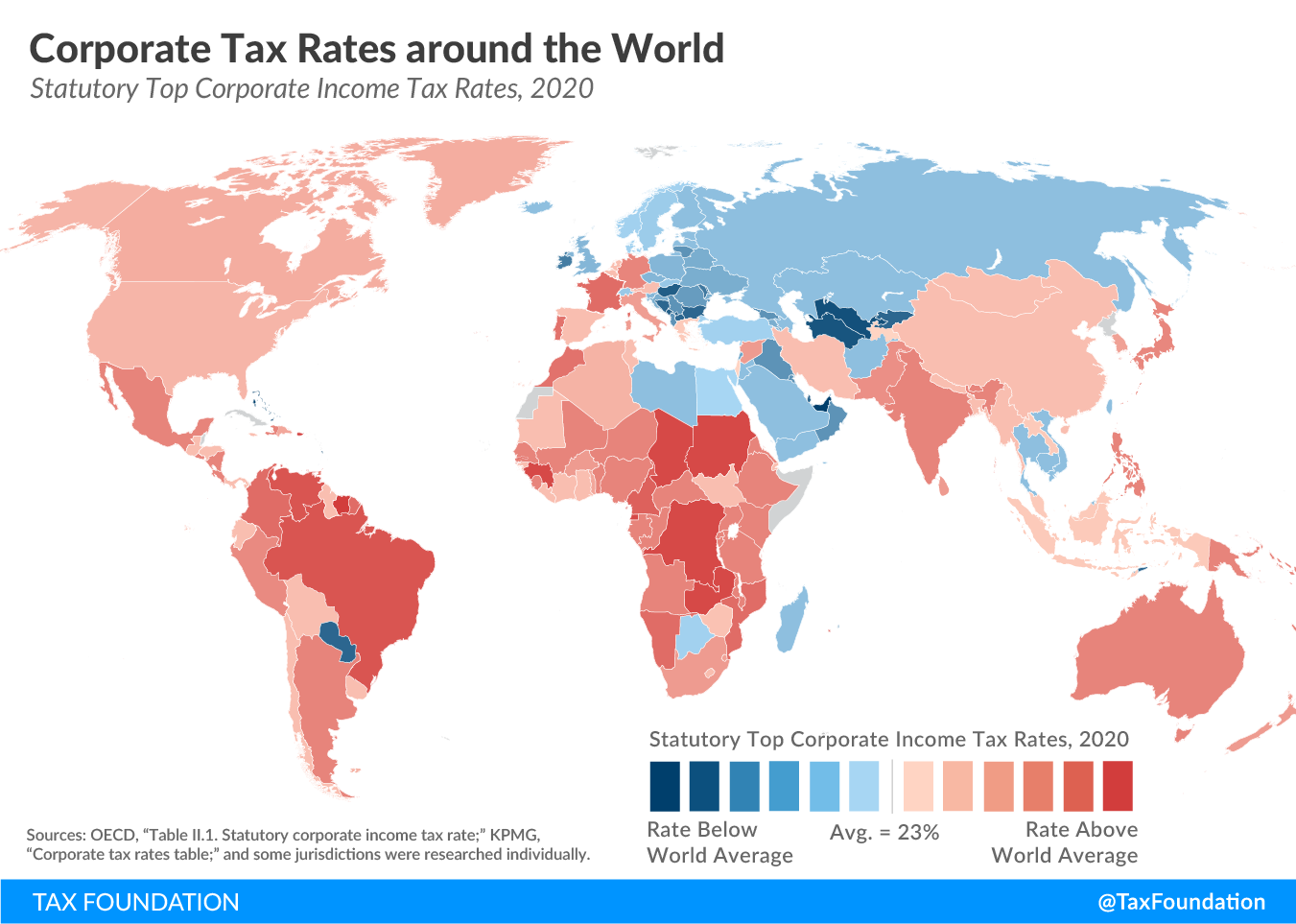

The Impact of Corporate Tax Rates on the Economy

Corporate tax rates play a crucial role in shaping business investments and economic growth. Lower tax rates, such as those introduced by the Tax Cuts and Jobs Act (TCJA) in 2017, were designed to stimulate the economy by encouraging firms to reinvest profits back into their operations. Proponents argue that lower taxes lead to increased business investments, which can create jobs and enhance productivity. However, a significant concern among economists is whether these tax cuts have effectively translated into higher corporate tax revenue in the long run.

According to a recent study, the initial optimism surrounding tax rate reductions has tempered, as the expected surge in corporate tax revenue has not fully materialized. After the implementation of the TCJA, corporate tax revenue experienced a drastic decline, which was only reversed when companies began to report higher profits post-2020. This complex relationship between tax rates and corporate behavior showcases the need for ongoing assessment to ensure tax policies align with broader economic goals.

Frequently Asked Questions

What impact did the TCJA have on corporate tax rates and corporate tax revenue?

The Tax Cuts and Jobs Act (TCJA), passed in 2017, permanently reduced the U.S. corporate tax rate from 35% to 21%. This significant cut was projected to decrease federal corporate tax revenues by $100 billion to $150 billion annually for the next decade. Initially, corporate tax revenue saw a steep decline of 40% upon the law’s implementation, but it began to rebound by 2020, as business profits increased.

How did corporate tax cuts influence business investments according to recent studies?

Studies, including one by economist Gabriel Chodorow-Reich, indicate that corporate tax cuts under the TCJA stimulated an 11% increase in capital investments. Specifically, provisions allowing for immediate expensing of investments proved more effective than traditional rate cuts at prompting businesses to invest.

Are the benefits of corporate tax cuts to wages as significant as proposed?

The TCJA was initially projected to result in wage increases of $4,000 to $9,000 per worker annually. However, subsequent analyses estimate that the actual increase was closer to $750 per year. This discrepancy highlights the complexity and contentious nature of how corporate tax rates and business investments impact wage growth.

What alternatives exist for corporate tax reform beyond raising tax rates?

Instead of solely raising corporate tax rates, a potential solution discussed by economists is to reinstate expensing provisions that proved effective in encouraging investment. This approach could balance the need for increased revenue while fostering business growth and innovation.

What are the current debates surrounding corporate tax rates as they approach expiration in 2025?

As key provisions of the TCJA are set to expire in 2025, debates intensify over whether to raise corporate tax rates to support federal revenue or to extend existing cuts to stimulate economic growth. Politicians from both parties are leveraging this debate in their campaign strategies, emphasizing different interpretations of the law’s economic effects.

How has the perception of corporate tax rates evolved since the TCJA’s implementation?

The perception of corporate tax rates has shifted, with many acknowledging that while tax cuts were intended to spur growth and investment, the dramatic drop in tax revenues raised questions about their long-term effectiveness. This change is prompting calls for a reevaluation of the corporate tax structure as policymakers consider future reforms.

What is the relationship between corporate tax rates and the Child Tax Credit?

The debate over corporate tax rates often intersects with discussions about the Child Tax Credit, particularly regarding funding for social programs. Advocates for raising corporate tax rates argue that increased revenues could support the expansion of credits like the Child Tax Credit, which directly benefits low- and middle-income families.

How do corporate tax cuts correlate with overall economic growth?

The relationship between corporate tax cuts and economic growth remains contested. While proponents argue cuts boost business investments that ultimately benefit the economy, critics highlight that the resultant drop in corporate tax revenue may hinder public services and investments, questioning the net positive impact of lower corporate tax rates.

| Key Points |

|---|

| Corporate tax rates are a contentious topic in U.S. politics, especially with the upcoming expiration of parts of the 2017 Tax Cuts and Jobs Act (TCJA). |

| The TCJA reduced corporate tax rates from 35% to 21%, significantly impacting federal tax revenues projected to decrease by $100-$150 billion annually. |

| Debates among politicians show a division: Democrats favor raising rates to fund services, while Republicans argue for further reductions to stimulate growth. |

| Harvard economist Gabriel Chodorow-Reich’s study shows limited wage growth and business investment from the TCJA’s corporate cuts, prompting calls for thoughtful policy evaluations. |

| Chodorow-Reich suggests reinstating expensing provisions alongside potential rate increases as a way to raise revenue while promoting economic growth. |

| Although corporate tax revenue plummeted immediately post-TCJA, it rebounded significantly by 2020 due to increased business profits, highlighting the complexity of corporate taxation effects. |

Summary

Corporate tax rates are crucial in determining the financial landscape for businesses and influencing overall economic growth. As Congress prepares for a tax debate in 2025, the implications of the 2017 TCJA are at the forefront of discussion. While some advocate for raising corporate tax rates to enhance public revenue and service funding, others argue that lower rates foster business investment and economic stimulation. Understanding the multifaceted impacts of these tax policies, particularly regarding revenue and wage growth, is vital for making informed legislative decisions that will affect the U.S. economy in the coming years.